Most of us have been experiencing unexpectedly cold temperatures and high rainfall lately but the good news is that spring is on the way. As the days grow longer and warmer, there can be a sense of optimism and a feeling of renewal.

Market watchers, investors and mortgage holders, who’d been anxiously awaiting the release of the latest inflation data at the end of July, could neither jump for joy nor collapse in despair.

The best that could be said about the figures was that they were not as bad as they could have been. It remains to be seen how the Reserve Bank board will view inflation’s modest increase when it meets on August 5 and whether it decides on an interest rate rise to counter it. The Australian Bureau of Statistics says prices rose 1% in the June quarter and 3.8% annually.

Retail sales continue to splutter along with the latest data showing a 0.5% increase in sales in June thanks to the sales but over the quarter, retail sales volumes fell 0.3% for the sixth time in the past seven quarters. Meanwhile, building approvals fell 6.5% in June after a 5.7% rise the previous month.

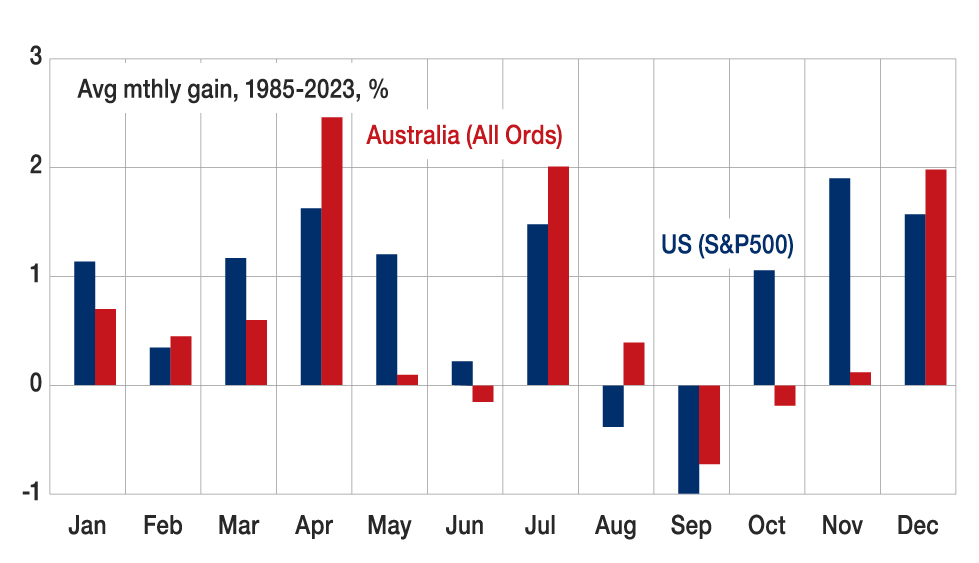

The ASX S&P 200 index finished the month strongly with an increase of around 4%, riding out a mid-month plunge. But the currency didn’t fare quite as well, falling below US65 cents for the first time in almost three months. In the US, the S&P 500 finished the month almost where it began after a big mid-month upward spike then fall but, for the year to date, it’s recorded an increase of almost 15%.

Market movements and review video – August 2024

Stay up to date with what’s happened in markets and the Australian economy over the past month.

While the anxiously awaited release of the latest inflation data at the end of July, showed an increase, it was in line with economists’ predictions.

Given the RBA wants inflation back within a 2-3% target range by the end of 2025, there were concerns about the inflation figures and the implications for the cash rate.

The ASX finished the month strongly with an increase of around 4%, riding out a mid-month plunge and surging to a record high for the ninth time this year. Click the video below to view our update.

When passion is the purpose of investing

Investing is often considered best undertaken with a cool head and heart. But for some investors, passion is the whole purpose of the investment.

Passion investing is what it sounds like – investing in things you love, non-traditional assets that generally allow you to enjoy ownership while hopefully watching them appreciate in value at the same time.

Most traditional investments take into consideration time horizon, risk appetite and investment capital appreciation goals. For the passion investor, while financial considerations may dictate their investments to some extent, they are strongly influenced by more than market returns and want to invest – and collect – in a way that supports their interests and passions.

The growth of passion investing

We Australians certainly love collecting and, according to the eBay State of Collectibles report, we also care about the financial implications of our collections. In fact, more than one in four Aussies collect goods such as coins, toys, sneakers and art and more than 40% of those collectors could be considered passion investors as they have a financial objective in mind.

The top 10 luxury passion investments

While buying and selling on Ebay is one end of the scale, the other end of the scale is the luxury passion investments. For those who have the cash to splash, some high-end investments can prove very lucrative.

According to Knight Frank’s Luxury Investment Index, the top 10 most successful passion investments ranked in order from those recording the highest returns are art, jewellery, watches, coins, coloured diamonds, wine, furniture, luxury handbags, classic cars and rare whisky.i While major auction houses recorded record sales last year, the Luxury Investment Index recorded a marginal decline of -1%, largely due to a drop in the rare whisky index of -9%. This overall decline was on the back of an impressive 16% increase the previous year, highlighting the volatility of the index.

Art typically records the most gains as investors pay stellar prices for museum quality works of art, with several single owner collections producing totals in excess of US$2.5 billion. It’s not just art setting records though. A US$143 million Mercedes-Benz Uhlenhaut Coupé set a new record for the most expensive car ever sold, with the most expensive watch, a 1957 Patek Philippe 2499, going for almost $10 million dollars.

Exploring other passions

Of course, passion investing is more than just the above luxury goods. If you thought Lego was just a toy that possesses enduring popularity, think again – the biggest online database for collectible Lego sets is now worth $1.2bn and it is possible for investors to realise profits in the range of 150% to 250%.ii

Following in Lego’s footsteps as a popular passion investment is sneakers. More than just comfy footwear to collectors, sneaker reselling has become a $6 billion industry globally, with the most sought-after limited-edition shoes commanding six-figure prices on the resale market.iii

Things to consider

While collecting items you love may seem like an exciting way to park some extra capital, passion investing can be a risky proposition and there are a number of things to consider.

Passion investments can be extremely susceptible to fluctuations in their value and luxury niche items can be hard to sell during economic downturns.

You have to know what to look for and it can be difficult, if not impossible, to predict what will be of interest to collectors in years to come. As with more traditional investments, you usually need to hold on to passion investments for some time in order for their value to grow so they are rarely a ‘get rich quick’ scheme.

They are also called passion investments for a reason. Any investment you are strongly attached to can potentially cloud your judgment when making decisions about buying, selling, or holding onto them.

You also need to think about where and how your objects are stored so they don’t lose value and insurance is a consideration when you possess items of significant value.

If you enjoy owning things that bring you joy, by all means pursue your passions – that’s what life is all about after all. Just approach with caution when mixing passion with investing.

i https://www.knightfrank.com.au/blog/2024/04/04/art-leads-knight-franks-luxury-investment-index-with-prices-rising-11-in-2023

ii https://www.wsj.com/video/series/in-depth-features/lego-investing-is-booming-heres-how-it-works/5F2B44FE-2789-46E2-B280-9CA089EAB458

iii https://www.firstonline.info/en/sneakers-da-collezione-una-folle-ossessione-chi-ci-guadagna/

Going for Gold

Gold fever is in the air and it’s not just the prospect of medals at the upcoming Paris Olympics.

Gold prices have been climbing strongly in 2024 as investors, jittery about the effects of wars in the Middle East and Ukraine, buy up the asset because of its reputation as a safe haven. The spot price has risen more than 18 per cent since mid-February.i

Demand for the precious metal is also being driven by central banks adding to their gold reserves to hedge against currency and other market risks.

For investors, gold has been an alluring buy for centuries thanks to its association with wealth and power. As a precious metal and a physical asset, it often attracts a certain confidence, which is sometimes misplaced.

Patchy performance

Day traders might be lucky enough at times to buy or sell gold for a decent profit by correctly guessing when to get in or out but, generally speaking, gold is not an easy investment to love.

Over the longer term, it hasn’t always beaten inflation, the price can plunge at a time when market conditions suggest it should be rising and its performance against stocks and bonds has been varied.

In fact, there have been long periods of persistently low prices. It languished for around six years from 1988 before recovering and then again for the decade or so leading up to the beginning of COVID-19 in 2020. The uncertainty of the pandemic-era helped spark a rally that has increased the price by almost 38 per cent.

Pros and cons

So, is gold worth considering as part of a portfolio? As with any investment, there are pros and cons.

Like many other asset classes, gold can help to diversify a portfolio and reduce certain risks. During stock market downturns, gold prices often (but not always) begin to rise. Some investors like the idea that it is a scarce, physical asset and, despite its ups and downs, gold has tended to hold its value over time.

At times gold has provided a good hedge against inflation. For example, in the US between 1974 and 2008, there were eight years when inflation was high and during those times, gold prices rose by an average of 14.9 per cent annually.ii But different periods give different results. While US CPI growth was around 6.8 per cent in 2021 and 2022, gold prices were achieving an annual increase of just over 1 per cent.

How to invest

You don’t need to lug home gold bars and hide them under the bed to have a stake in a gold investment.

Of course, it is possible to own gold bullion by buying online or in person from one of a number of registered dealers in Australia. The actual gold can be delivered to you or held in storage for a fee. You could also own physical gold by buying jewellery although there are high mark ups and resale value isn’t assured.

The ASX provides the avenue to buy shares in one or more of the many gold mining companies. You’ll need to do your homework carefully to consider the credentials of the companies. Some are riskier than others depending on the countries in which they operate and their size.

You could also consider exchange traded funds (ETFs) that are linked to or track the gold price. One advantage is provided by funds that hedge currency risk so that your returns won’t be affected by differences in the US dollar. Although with any fund, you’ll need to factor in an annual management fee, which will reduce your ultimate return.

If you’re interested in achieving a balanced portfolio, we’d be happy to help you.i Gold – Price – Chart – Historical Data – News (tradingeconomics.com)

ii Is Gold An Inflation Hedge? – Forbes Advisor

To sell or not to sell is the question for moving into aged care

Moving into residential aged care can trigger a range of emotions, particularly if it involves the sale of the family home.

What is often a major financial asset, is also one that many people believe should be either kept in the family or its value preserved for future generations.

Whether or not the home has to be sold to pay for aged care depends on a number of factors, including who is living in it and what other financial resources or options are available to cover the potential cost of care.

It also makes a difference if the person moving into care receives Centrelink or Department of Veterans Affairs payments.

Cost of care

Centrelink determines the cost of aged care based on a person’s income and assets.i

For aged care cost purposes, the home is exempt from the cost of care calculation if a “protected person” is living in it when you move into care.

A protected person could be a spouse (including de facto); a dependent child or student; a close relative who has lived with the aged care resident for at least five years and who is entitled to Centrelink income support; or a residential carer who has lived with the aged care resident for at least two years and is eligible for Centrelink income support.ii

Capped home value

If the home is not exempt, the value of the home is capped at the current indexed rate of $201,231.iii

If you have assets above $201,231 – outside of the family home – then Centrelink would determine you pay the advertised Refundable Accommodation Deposit (RAD) or equivalent daily interest rate known as the Daily Accommodation Payment (DAP), or a combination of both.

The average RAD is about $450,000. Based on the current interest rate of 8.36% [note – this is the rate from July 1] the equivalent DAP would be $103.07 a day.

Depending on your total income and assets, you may also be required to pay a daily means tested care fee. This fee has an indexed annual cap of $33,309 and lifetime cap of $79,942.

This is in addition to the basic daily fee of $61.96 and potentially an additional or extra service fee.

There is no requirement to sell the home to pay these potentially substantial costs, but if it is a major asset that is going to be left empty, it may make sense.

Other options to cover the costs may include using income or assets such as superannuation, renting the home (although this pushes up the means tested care fee and can reduce the age pension) or asking family to cover the costs.

Centrelink rules

For someone receiving Centrelink or DVA benefits, there is an important two-year rule.

The home is exempt for pension purposes if occupied by a spouse, otherwise it is exempt for up to two years or until sold.

If you are the last person living in the house and you move into aged care and still have your home after two years, its full value will be counted towards the age pension calculation. It can mean the loss of the pension.

Importantly, money paid towards the RAD, including the proceeds from a house, is exempt for age pension purposes.

Refundable Deposit

As the name suggests, the RAD is fully refundable when a person leaves aged care. If a house is sold to pay a RAD, then the full amount will ultimately be paid to the estate and distributed according to the person’s Will.

The decisions around whether to sell a home to pay for aged care are financial and emotional.

It’s important to understand all the implications before you make a decision.

Please call us to explore your options.

i https://www.myagedcare.gov.au/understanding-aged-care-home-accommodation-costs

ii https://www.myagedcare.gov.au/income-and-means-assessments

iii https://www.myagedcare.gov.au/income-and-means-assessments